In this third and final part of Step 6, Don introduces the final checking account in the Playbook, the Investment Holding Account, as the place to collect the money that is the reason you started your business in the first place. This account grows the personal capital you can use to buy assets to make money without you even having to work.

After establishing your cash flow plans by the Playbook and adding this fifth and final account, your business will be set up to build wealth for you and your family.

Your Business Profit Account – Setting a High-Water Mark

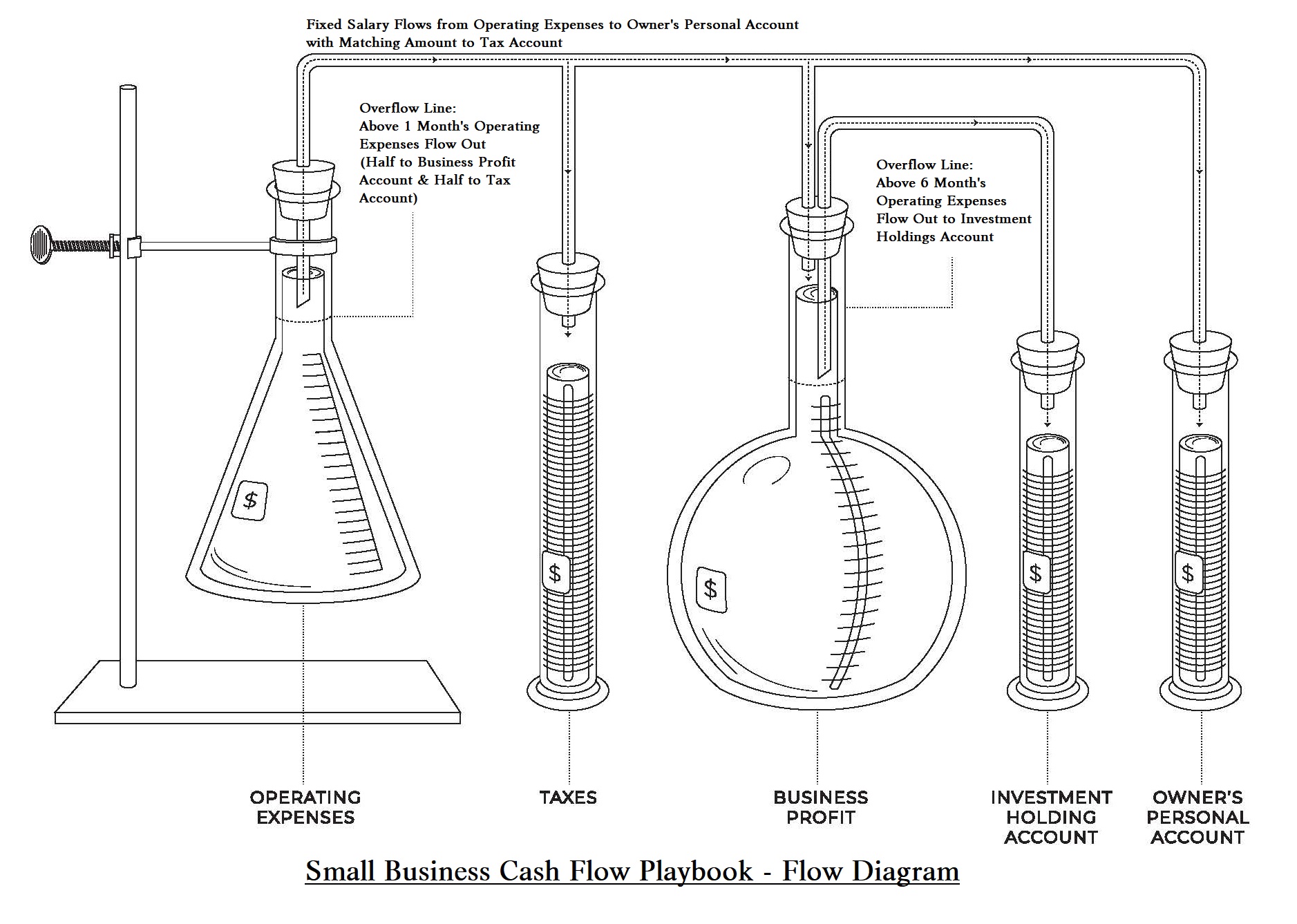

When you set up your Profit Account, you establish a visible representation of the “extra” dollars produced by your business beyond one month of the operating expenses in your Operating Account. It’s motivating to see the Profit Account grow, as you know you’re building a buffer into your financial life.

Once your Profit Account reaches the equivalent of six months of operating expenses, your safety net is well-positioned for unforeseen challenges. If necessary, you could operate your business without any sales for six months. That’s a huge accomplishment! Once you hit that threshold, the Playbook guides you to set up your final checking account, your Investment Holding Account. Any amount in your Profit Account above that six-month high-water mark should get swept into your Investment Holding Account. This time, you don’t have to split the amount you’re transferring with your Tax Account, as you’ve already got that covered when you first moved it out of your Operating Account. The following flow chart can help show the flow of money, now that we’ve described all the accounts of the Playbook.

The Investment Holding Account – A Big Goal of Your Business

The Investment Holding Account is the pinnacle of financial foresight in the Playbook. As funds exceeding the high water in your Profit Account “boil over” into your Investment Holding Account, you’ll start to see the realization of one of the ultimate goals of starting your business: building wealth toward financial freedom. The dollars growing in your Investment Holding Account, while maintaining a solid safety net in your Profit Account are a new opportunity for you. While it’s tempting to spend these extra “above and beyond” dollars on fun things like big toys, a new house, or an exciting vacation, the Playbook encourages you to invest them instead. Use these funds to invest in assets that make you money without you having to work for it. There are a variety of ways to invest that will provide a return, and the Playbook suggests that once the assets in the Investment Holding Account provide that return, you will have financial resources to spend on those fun things. That way, your investments will continue to regenerate for you month in and month out.

Your Investment Goals

As you install the Playbook into your business and your Profit Account begins to grow, it’s important to consider your Investment Goals and an Investment Plan, even before you reach the point of starting to put money into your Investment Holding Account. By having a vision of what you want to achieve with your accumulated wealth, you’ll be even more motivated to grow your business further.

Your goals can include a wide variety of items from fun items or experiences to charitable contributions or other ways to give back. Writing out your desired goals is important because doing so makes your vision more concrete. Ensure the list contains what you find most important or meaningful to you, as it will both motivate you and add a sense of accomplishment when you reach those goals.

Your Investment Plan

While your Investment Goals provide the target, your Investment Plan will keep you on track to achieve them. It’s easy to get distracted or jump the gun when dollars start showing up in the Investment Holding Account. That’s a big reason why the word “Holding” is in the title! Holding your investments allows them to grow. Instead of using the investments themselves, you can use the returns of those investments as the funds to spend on any of your Investment Goals that require dollars to achieve. That way, you’ll continue to have future opportunities while maintaining investments that continue to provide returns. Obviously, there are many kinds of investments you can make and we won’t make specific recommendations here.